Bitcoin's Buyer Base Is Shrinking

Three buyers are holding the entire market together. Everyone else is leaving. Bitcoin hasn't broken $65,400 during six weeks of war. But the reason it's holding isn't bullish. It's structural, fragile, and dependent on a handful of mandated buyers.

Bitcoin closed the week near $73,000, up roughly 7% as the ceasefire rally pushed it from $68,000 to its highest level since late March. The S&P 500 posted its best week since November. Oil dropped 12%. On paper, it looks like relief.

It isn't. The Islamabad peace talks collapsed after 21 hours on Sunday. The Strait of Hormuz is still closed. And the buyer structure underneath Bitcoin is the most concentrated it has ever been.

The floor is real. The reason it's holding is the problem.

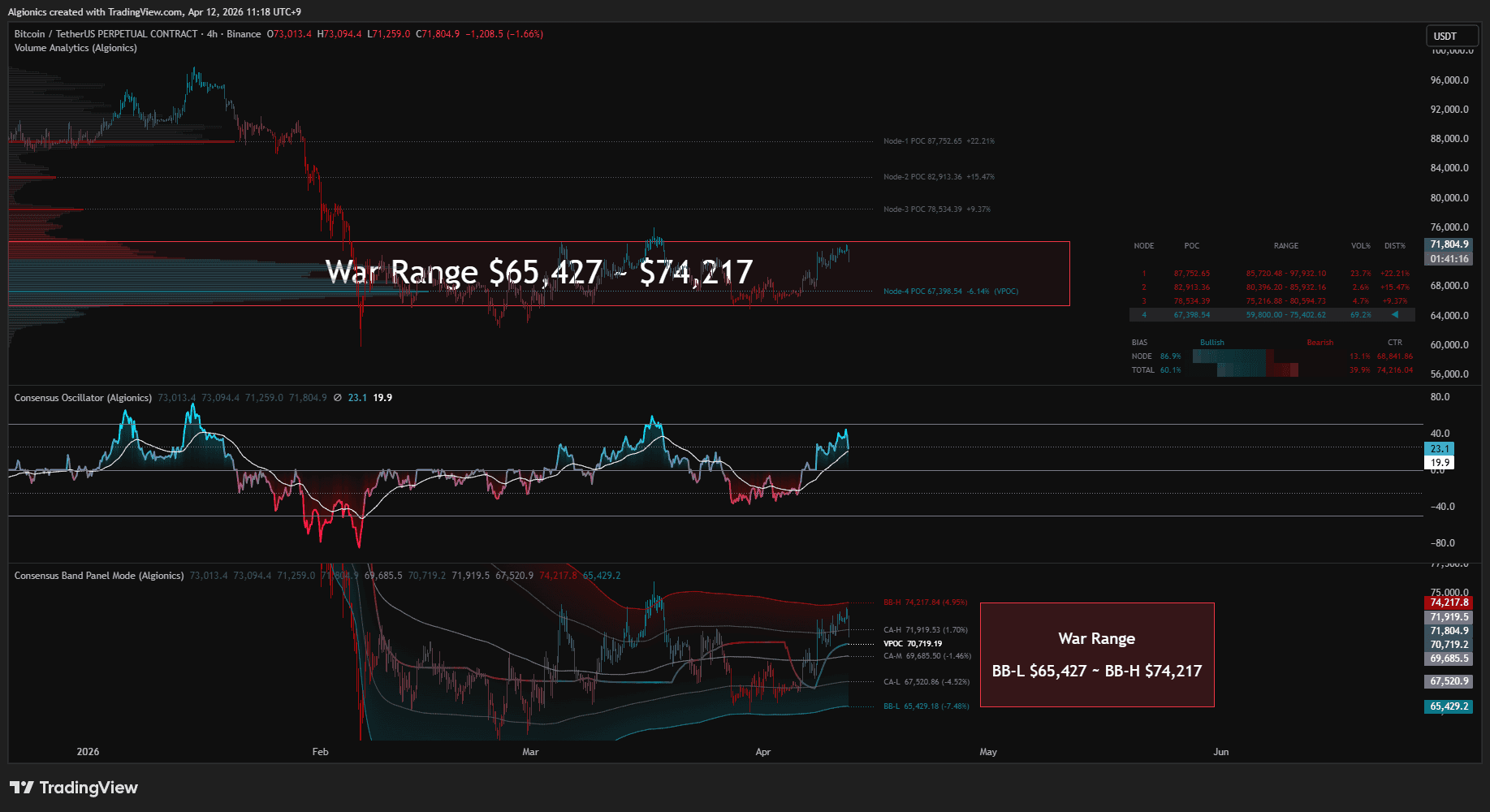

Bitcoin has traded in a $65,400 to $74,200 range for the entire six weeks of the Iran war. That kind of stability during a global energy crisis seems impressive until you look at who is actually buying.

U.S. spot ETFs have absorbed roughly 50,000 BTC per month since the war started. Strategy (formerly MicroStrategy) has added another 44,000 per month, bringing total holdings to 766,970 BTC at a blended cost basis of $75,644. Their latest purchase on April 5 was 4,871 BTC at $67,718, pulling the average lower.

Between those two channels, roughly 94,000 BTC per month is being bought by entities that are structurally mandated to buy. ETFs buy when inflows come in. Strategy buys as long as STRC preferred equity demand holds. Neither is making a discretionary call on the market. They're executing a process.

Everyone else is selling.

Whales holding 1,000 to 10,000 BTC have completed one of the most aggressive distribution cycles on record. The one-year change in whale holdings has swung from positive 200,000 BTC at the October 2025 peak to negative 188,000 BTC today. That's a nearly 400,000 BTC reversal in about 18 months.

Mid-tier holders (100 to 1,000 BTC) haven't flipped to selling yet, but their buying pace has collapsed over 60%. Annual additions dropped from nearly 1 million BTC to 429,000. The trajectory is clear.

Listed miners are liquidating treasuries. Riot Platforms, MARA Holdings, and Genius Group disclosed selling more than 19,000 BTC in a single week earlier this month. Bhutan's sovereign holdings dropped from 13,000 BTC to 3,954, a 70% reduction in 18 months.

CryptoQuant's 30-day apparent demand metric sits at negative 63,000 BTC. The broader market is selling faster than institutions can absorb.

The ceasefire rally was a short squeeze, not a structural shift.

Tuesday's ceasefire announcement triggered BTC's sharpest single-day rally in over a month. $600 million in crypto futures got liquidated, mostly shorts. Open interest in BTC and ETH perpetuals expanded by $2.1 billion and $2.2 billion respectively in 24 hours, with coin-denominated OI also rising, confirming net new long positions rather than just short liquidations.

The Coinbase Premium turned positive for both BTC and ETH for the first time since October's all-time high. That's the first real sign of U.S. demand in months. But one day doesn't reverse a structural trend.

By Friday, the rally had stalled. BTC traded sideways around $72,000 as the CPI print came in at 3.3% headline (driven by a record 21.2% monthly gas price surge) with a tamer 0.2% core. The market digested the number without panic, but the inflation story is far from over. Energy costs take months to filter through supply chains.

Then Sunday happened. The Islamabad talks ended with no deal. Vance called it "our final and best offer." Iran blamed "excessive demands." The nuclear issue remains unresolved. The ceasefire itself is now in question.

What this structure actually means.

The number of entities providing sustained buying pressure for Bitcoin can be counted on one hand. Strategy, ETFs, and to a lesser extent Morgan Stanley's new advisory channel. That's it.

This concentration has a ceiling problem. At $74,200, the mandated buyers have been enough to absorb discretionary selling. But they haven't been enough to push price higher. BTC has tested the top of this range multiple times during the war and failed every time.

The bull case is that if geopolitical risk fades and discretionary buyers return, the compressed range breaks upward with force, because there's very little supply left on exchanges (10-year lows in exchange balances). The bear case is simpler: if ETF inflows slow or STRC demand drops, the only consistent bid disappears, and there's nothing behind it.

This isn't a market making a directional call. It's a market being held in place by mechanics while everyone with a choice is walking away. Whether that floor holds depends entirely on whether the mandated buyers stay mandated.

Free on TradingView

What are you still configuring?

While others sell you "highly customizable" and leave you with endless settings to figure out, we eliminated all of them and called it "engineering".

ARES Generation 1

Coming April 22.

Latest

Ready to begin?

A precise tool for those who've already decided how they trade.