The Wire

Coverage

AAPL

Apple Inc.

NASDAQ

|

Tech

Published

COMPANY OVERVIEW

Apple designs, manufactures, and markets smartphones, personal computers, tablets, wearables, and accessories. The company also operates a growing services ecosystem including the App Store, Apple Music, iCloud, Apple TV+, and Apple Pay. iPhone remains the primary revenue driver at approximately 52% of total sales, followed by Services at 26%. Services carries significantly higher margins and has become the key growth engine.

VALUATION SNAPSHOT

P/E (TTM)

33.9

5Y avg:

29.7

Forward P/E

32.8

-

PEG

2.52

10Y med:

1.70

D/E

0.80

-

| Quarter | Price | Fair Value | Gap |

|---|---|---|---|

| Q3 FY2023 | 191.33 | 155.50 | +23.0% |

| Q4 FY2023 | 173.75 | 152.41 | +14.0% |

| Q1 FY2024 | 192.53 | 155.52 | +23.8% |

| Q2 FY2024 | 171.48 | 156.52 | +9.6% |

| Q3 FY2024 | 210.62 | 160.46 | +31.3% |

| Q4 FY2024 | 227.79 | 167.69 | +35.8% |

| Q1 FY2025 | 255.59 | 164.04 | +55.8% |

| Q2 FY2025 | 217.90 | 158.67 | +37.3% |

| Q3 FY2025 | 201.08 | 158.18 | +27.1% |

| Q4 FY2025 | 255.46 | 170.34 | +50.0% |

| Q1 FY2026 | 273.40 | 197.37 | +38.5% |

| Q2 FY2026 | 248.80 | 207.50 | +19.9% |

Current Fair Value

Apple's trailing fair value stands at $207.50 as of Q2 FY2026, based on a blended DCF and EPS multiple model. The stock closed the quarter at $248.80, a 19.9% premium to our estimate.

12-Quarter History

Over the past 12 quarters, Apple has consistently traded above its model fair value, with an average premium of 30.5%.

The gap narrowed to its lowest point in Q2 FY2024 at 9.6%, when macro uncertainty and iPhone cycle concerns weighed on the stock. It peaked at 55.8% in Q1 FY2025, driven by record holiday quarter results and AI integration expectations.

Why the Gap Is Narrowing

The current 19.9% premium is below the 12 quarter average. Two factors explain this compression.

First, fair value itself rose sharply from $170.34 in Q4 FY2025 to $207.50, reflecting accelerating FCF and EPS growth across the last two quarters. Second, the stock pulled back from its Q1 FY2026 high near $273 as tariff concerns and memory supply constraints tempered near term expectations.

What the Price Implies

For $248.80 to be justified by fundamentals alone, Apple would need to sustain approximately 18% annual earnings growth over the next five years.

The consensus expects roughly 14% for FY2026 and 9.5% for FY2027. Whether the gap between market expectations and consensus estimates closes through execution or correction is the central question for the next several quarters.

Fair value is derived from a 60/40 blended model combining a 2-Stage DCF (TTM FCF $129.2B, 10% growth based on 5-year average, 9.5% WACC, 3% terminal rate) with an EPS multiple approach (TTM EPS $8.26 at 28x, the 5-year median P/E). Net cash of $62B and 14.67B diluted shares are applied.

FINANCIAL SUMMARY

Annual Summary

(Annual In $B)

383.3

391.0

416.2

460.0

114.3

123.2

133.1

152.0

97.0

93.7

112.0

128.0

29.8%

31.5%

32.0%

33.0%

$6.13

$6.08

$7.46

$8.50

Revenue

Apple delivered record full-year revenue of $416.2B in FY2025, accelerating to 6.4% YoY growth after a modest 2.0% increase in FY2024.

The growth was broad-based, with iPhone, Mac, and Services all posting double-digit gains. Services crossed the $100B annual revenue milestone for the first time, growing 14% YoY on a purely organic basis.

Profitability

Operating income expanded steadily from $114.3B to $133.1B over the three reported fiscal years. Operating margin widened from 29.8% to 32.0%.

This margin expansion was driven primarily by the increasing Services mix, which carries significantly higher gross margins than hardware.

Earnings and Capital Return

EPS growth outpaced revenue growth due to margin expansion and continued share buybacks. FY2025 EPS of $7.46 represented a 22.7% YoY increase, compared to a slight decline in FY2024 when one-time tax charges depressed net income.

Apple returned over $110B to shareholders in FY2025 through buybacks and dividends.

Forward Estimates

FY2026E consensus projects revenue at $460.0B (+10.5% YoY) and EPS at $8.50 (+13.9% YoY), supported by the iPhone 17 cycle and further Services growth.

Operating margin is expected to reach 33.0%, extending the multi-year expansion trend.

Quarterly Summary

(Quarterly In $B)

Revenue Acceleration

Apple posted four consecutive quarters of strong YoY revenue growth: Q3 FY2025 at +10%, Q4 FY2025 at +8%, Q1 FY2026 at +16%, and Q2 FY2026 at +17%.

The Q1 FY2026 December quarter was the strongest, driven by the iPhone 17 launch cycle that delivered an all-time iPhone revenue record of $85.3B (+23% YoY) and pushed total revenue to $143.8B.

Margin Expansion

Operating margin expanded from 30.0% in Q3 FY2025 to 35.4% in Q1 FY2026, supported by a richer Services mix and gross margin reaching 48.2%. Q2 FY2026 gross margin further improved to 49.3%, a new record.

Services revenue has set all-time records in each of the last four quarters, crossing $30B quarterly for the first time in Q1 FY2026 and rising to $31.0B in Q2.

Earnings

EPS peaked at $2.84 in Q1 FY2026 (+19% YoY), reflecting both margin expansion and ongoing buybacks.

Q2 FY2026 EPS of $2.01 (+22% YoY) set a March-quarter record despite normal seasonal decline from the holiday peak.

Forward Outlook and Risks

Apple guided Q3 FY2026 revenue growth of 14% to 17% YoY, well above consensus expectations of 9.5%. This suggests iPhone 17 demand momentum continues.

Key risks for the forward estimate include rising memory costs, which Apple flagged as an increasing headwind, and supply constraints on advanced 3nm nodes at TSMC. The CEO transition from Tim Cook to John Ternus, effective September 2026, adds a governance variable but was received positively by the market.

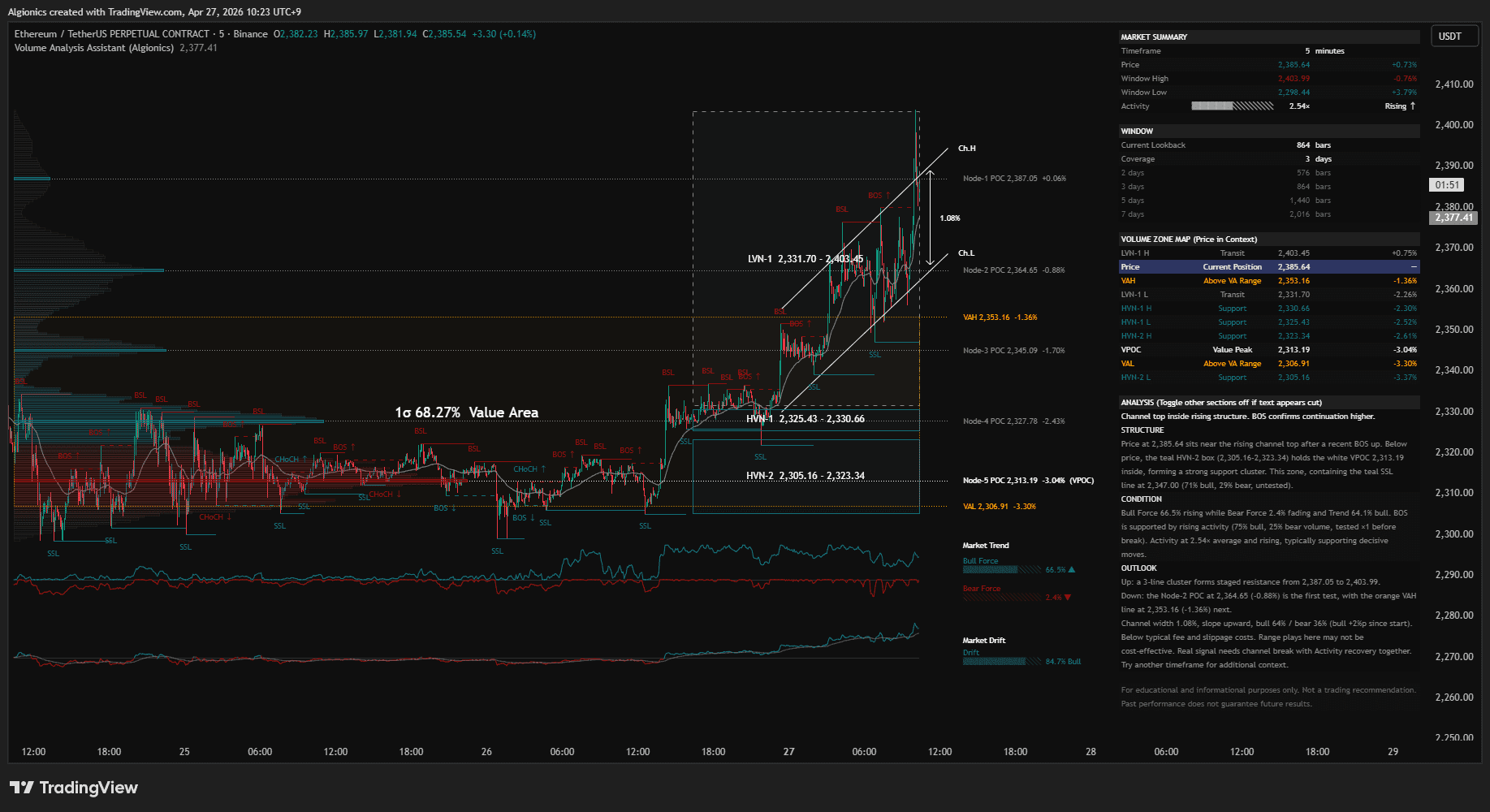

MARKET STRUCTURE

Price Location

Price at $280.14 sits in the upper part of the LVN-1 gap, a transit zone spanning $199.98 to $287.41. This places it between the Value Area below and the channel high above.

Below price, the HVN-2 box ($159.92 to $185.36) holds the VPOC at $172.17 inside, forming a strong support cluster. The HVN-1 box ($190.11 to $198.30) provides a secondary support shelf closer to the current level.

Trend and Momentum

Bull Force is at 40.8% and rising. Bear Force reads 0.0%. Trend is 40.8% bull.

Market Drift reads 97.0% bull, confirming the longer term directional bias aligns with the short term trend. Both measures point the same way, with no divergence between them.

Activity

Activity is at 0.70x average and recovering. Participation is returning but still subdued, sitting below the 1.0x threshold that would confirm institutional commitment at the current level.

This is the key variable. Directional conviction is present, but the energy behind it has not yet matched the positioning.

Resonance Channel

Channel width is 24.35%, slope upward. Bull/bear split is 55/45. Price is near the ceiling at $288.62 while the floor sits at $265.30.

The channel has been stable since its start, suggesting a structurally defined range rather than a breakout environment.

Resistance and Support

Looking up, a 3-line cluster forms staged resistance from $280.91 (BSL, tested once) to $288.62. This is the immediate barrier.

Looking down, the Node-1 POC at $272.65 (2.67% below) is the first support test. The Node-2 POC at $257.02 (8.25% below) follows. Both represent areas where volume previously concentrated.

Read

A sustained break above $287.41 with Activity expanding above 1.0x would confirm structural acceptance at higher levels. Without that volume follow-through, the current position near the channel ceiling is more likely to produce rotation back toward the channel floor.

Everything you see here

is one indicator.

From structure detection to analysis report, directly on your chart.

The Volume Analysis Assistant, available on TradingView.

STRUCTURE INTERPRETATION

Valuation and Structure Alignment

The valuation data and market structure point in the same direction.

Our blended model places Apple's trailing fair value at $207.50. The stock closed Q2 FY2026 at $248.80, a 19.9% premium. Over the past 12 quarters, the average premium has been 30.5%, meaning the current gap is narrower than usual.

This compression came from both sides. Fair value rose sharply from $170.34 in Q4 FY2025 to $207.50, reflecting accelerating FCF and EPS. The stock pulled back from its Q1 FY2026 high near $273 as tariff concerns and memory supply constraints tempered near term expectations.

Volume Structure at the Decision Point

The volume structure reflects this same tension. Price sits at $280.14, near the top of the Resonance Channel at $288.62, pressing against a 3-line resistance cluster.

Activity is at 0.70x and recovering but still below 1.0x. Institutional participation has not yet confirmed this level. Bull Force at 40.8% with Bear Force at 0.0% and Drift at 97.0% bull show directional conviction exists, but the energy to sustain a breakout has not arrived.

Two Scenarios

If Activity expands above 1.0x and price clears $287.41 with volume follow-through, the market is structurally accepting a higher range. The premium to fair value would widen, but supported by confirmed demand rather than speculation.

If Activity stays subdued and price fails at the channel ceiling, a rotation toward the Node-1 POC at $272.65 or the Node-2 POC at $257.02 becomes likely. The $257 level would bring the premium down to roughly 24%, closer to the 12 quarter average.

Fundamental Context

Q2 FY2026 delivered 17% revenue growth and 22% EPS growth, both above expectations. Apple guided Q3 revenue growth of 14% to 17%, well above the 9.5% consensus. The earnings trajectory is accelerating.

But the current price already reflects much of this optimism. For $280 to be justified by fundamentals alone, Apple would need to sustain approximately 18% annual earnings growth over five years. The consensus expects 14% for FY2026 and 9.5% for FY2027.

The Central Question

The question is not whether Apple is a strong business. It is whether the market has already priced in the strength.

The volume structure suggests the answer is being decided right now, at this channel ceiling, with Activity as the tiebreaker.

RISK FACTORS

Tariff and Trade Policy

Apple flagged tariff-related costs in both the March and June quarters. The Section 122 regime imposes a baseline cost on imported electronics, and Section 301 tariffs against China remain in effect.

Production diversification toward India is underway, but final assembly there still depends on Chinese-made subcomponents. If tariff rates escalate, Apple faces a choice between absorbing costs or passing them to consumers.

Regulatory and Antitrust

The European Commission has opened a formal noncompliance investigation under the Digital Markets Act, targeting App Store policies. In the US, the DOJ antitrust lawsuit is in the discovery phase.

The Google default search agreement, estimated at $20B annually in Services revenue, must terminate within one year of the December 2025 ruling. Any structural change to commissions or the loss of the Google payment could pressure Services margins by 100 to 150 basis points.

Supply Chain

Apple reported supply limitations on advanced node SoCs and memory components in Q2 and Q3 FY2026. Rising memory costs were cited as an increasing headwind.

TSMC's 3nm capacity allocation remains tight. Any disruption to this single-source dependency would directly impact product availability.

Revenue Concentration

iPhone remains approximately 52% of total sales. A slowdown in upgrade cycles from market saturation, Huawei competition in China, or consumer resistance to AI feature monetization would disproportionately affect top-line growth.

CEO Transition

Tim Cook steps down in September 2026, with John Ternus succeeding. The market received this positively, but execution continuity during the transition is not guaranteed.

For educational and informational purposes only. Fair value estimates are derived from a quantitative model and reflect calculations as of the stated publication date. They do not constitute investment advice or buy, sell, or hold recommendations. Past performance does not guarantee future results.

Your chart shows everything.

Except what it means.

This writes it out.

Directly on your chart. In plain language.

Market analysis and trade ideas. Have a ticker in mind? Send us your request.